MannyPay - Manny Open Questions

Competition is good, and any open and interoperable payment system should make it easy for new players, small and big, to join. In this spirit, I am happy that another e-wallet has entered the market: MannyPay.

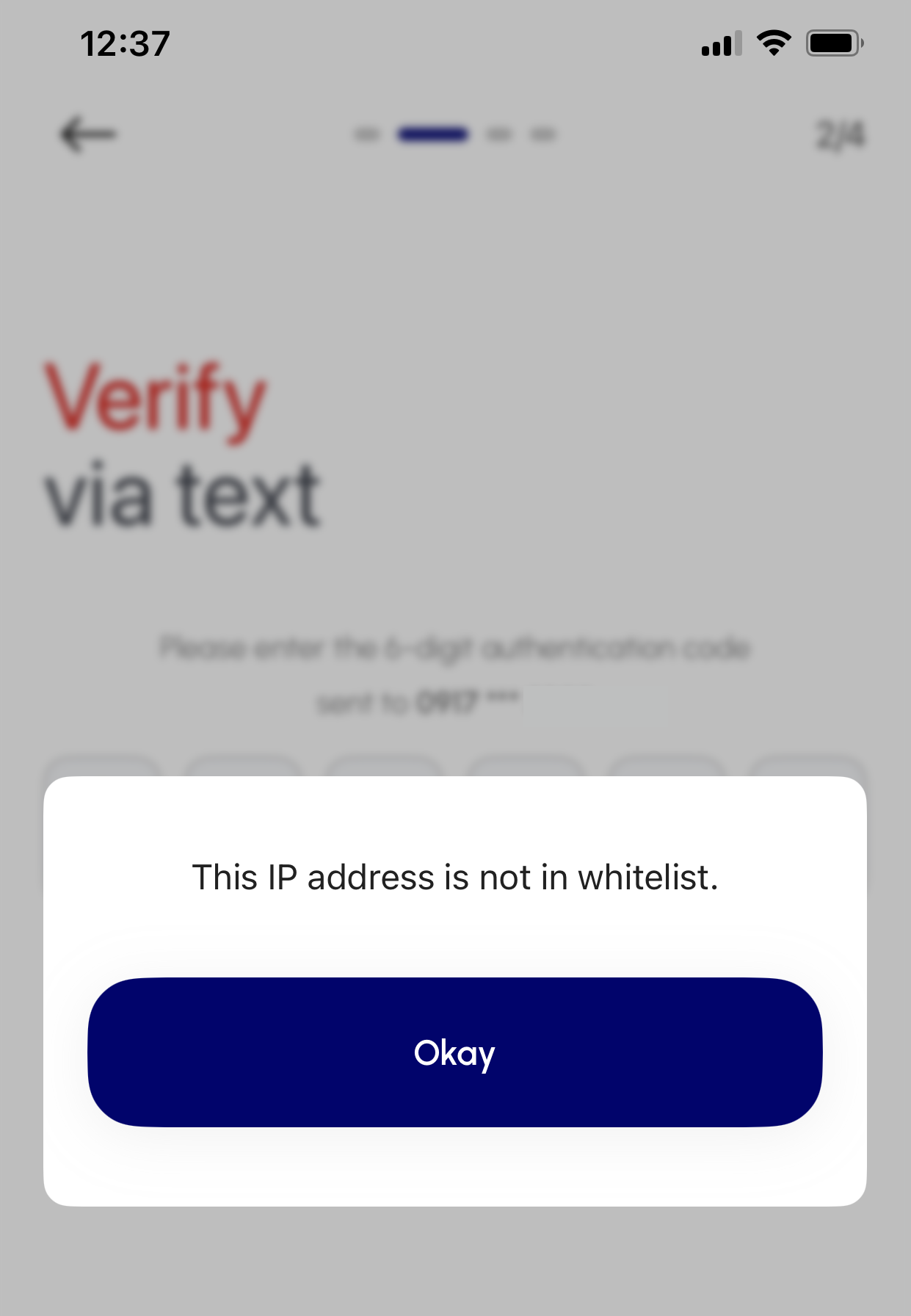

To satisfy my curiosity, I downloaded the app on my iPhone and tried to enroll. Unfortunately, I did not manage to get past a nonsensical error message, and the app froze on the screen where you are supposed to enter a passcode from a text message (which also never arrived).

Nevertheless, I have some initial comments, and I will update this post when they have fixed their teething issues.

Interchange and Surcharge

QR Payments - Innovate, don't imitate!

Instead of innovating payments, the new breed of QR/A2A payment schemes too often think of their system as a “primitive” form of card payments. Or, they treat payment merely as an enabler for their ambition of becoming a virtual bank. There is too much data, too much functionality and not enough effort to make the payment process better.

In this post, I want to make the case for removing data from QR payments.

In my view, the principles of any new payment system should be: “Payment moves money efficiently, anonymously and conveniently (for the customer). Use of account information is kept to a minimum. There should be no personal data.”

InstaPay or P2P QRPh? What is it?

In my previous post, I voiced my opinion that many merchants use their personal GCash account to accept payments. At that time, I was thinking of the proprietary GCash QR code that would only work for customers who use their GCash wallets. More recently, I noticed personal QR codes that seem to work with all e-wallets and mobile banking applications. I tested this specifically with the BPI banking application and the GCash wallet.

Have I found the P2P QRPh?

In this post, I am analyzing the data and the formatting that is used for the P2P QR code. If you are curious, you can also run your own QR codes through my QR Decoder.